Deep Dive: L'Oréal

Another premium/luxury quality stock

Introduction: From Eugène Schueller to Hieronimus, the engine of global beauty

Founded in 1909 by chemist Eugène Schueller with a single innovation—the first safe hair dye—L’Oréal has grown into the undisputed global leader in cosmetics. What began in a modest Parisian apartment has evolved into a €43.5 billion juggernaut present in 150 countries. Unlike Safran, whose identity is rooted in French defense and sovereignty, L’Oréal embodies something equally French but universally relevant: the democratization of beauty through science and accessibility. Yet like Safran, L’Oréal carries DNA forged in crisis and European aspiration: the DNA of a founder who believed science could empower ordinary people.

With over 90,000 employees worldwide, a market capitalization exceeding €200 billion, and 20% operating margins, L’Oréal is the world’s number one in beauty by an order of magnitude. Unilever, its nearest competitor, trails at €26 billion in revenues; Estée Lauder at €15 billion. No challenger comes close to L’Oréal’s scale, portfolio breadth, or profitability. The company controls over 42% of the global market by some measures, a position maintained not through predatory acquisition alone, but through relentless innovation and disciplined capital allocation.

The company’s trajectory mirrors the evolution of global consumer culture: from professional salons to department stores, from urban elites to emerging-market masses, from chemical complexity to “Beauty Tech” augmented by AI. L’Oréal has been at the center of each transition. And like Safran in defense, L’Oréal is a cultural export, a symbol of French elegance and scientific rigor projected onto five continents as soft power. Its continued dominance secures not just shareholder returns but also French influence in a category where consumption is global but heritage is local.

Corporate evolution: a portfolio architecture of disciplined luxury pluralism

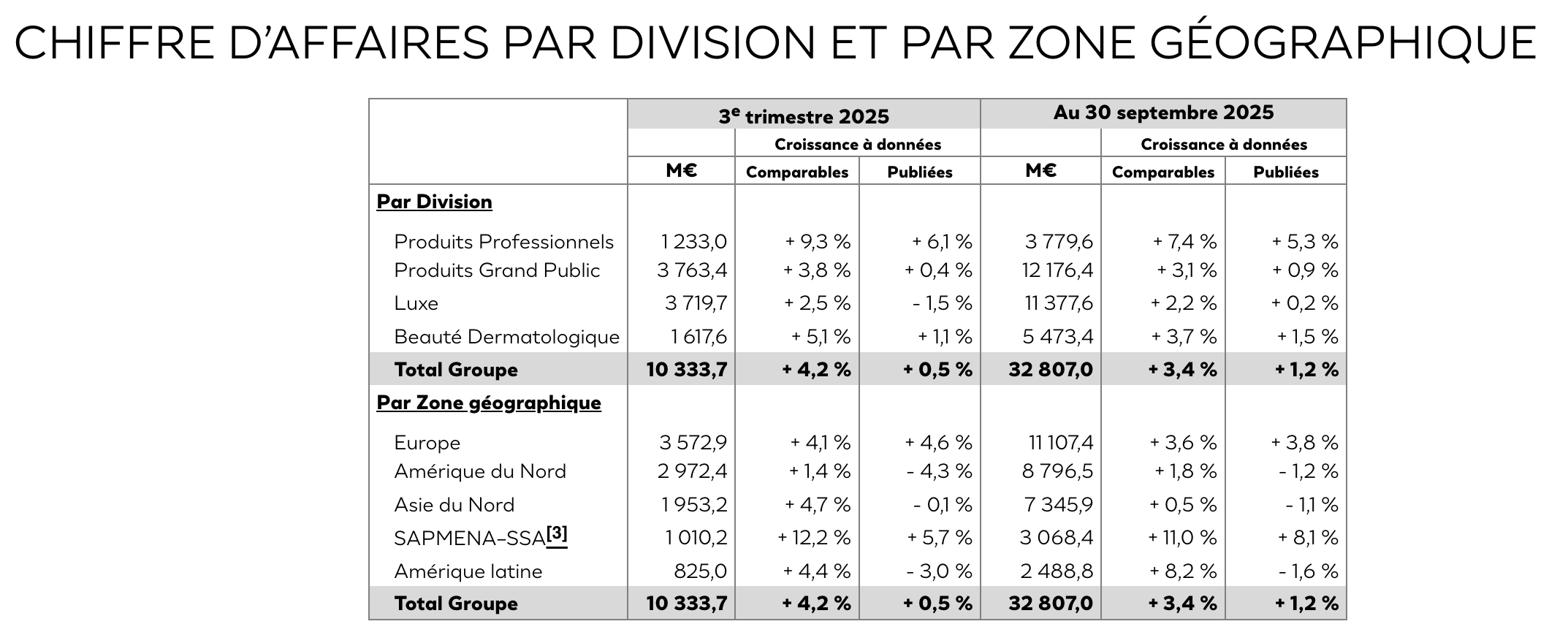

L’Oréal’s business model rests on what the company calls “universalization”, the idea that beauty is one, but the expression of it is diverse. This philosophy has led to a portfolio structure unmatched in complexity and reach. The group operates through four divisions, each with its own margin profile, growth dynamic, and customer base:

L’Oréal Luxe

L’Oréal Luxe (€15.59 billion in 2024 revenues, +4.5% growth, ~22% operating margin) is the crown jewel, housing Lancôme, Yves Saint Laurent Beauté, Giorgio Armani Beauté, Valentino, Prada, Ralph Lauren, and as of October 2025, Creed following the landmark €4 billion Kering Beauty acquisition. This division generates the highest margins and attracts the most affluent consumers, yet faces structural headwinds in North Asia where luxury-goods demand has softened post-pandemic.

Consumer Products

Consumer Products (€16 billion, +4.9% growth, 21.1% margin) is the breadth engine: L’Oréal Paris, Garnier, Maybelline, and Magic Mask serve mass markets across continents. Despite lower unit margins than Luxe, its volume and distribution reach make it the profit engine in absolute terms. Innovation here drives market share gains in key emerging markets, particularly Latin America and Southeast Asia where affordable premium is the growth vector.

Dermatological Beauty

Dermatological Beauty (€7 billion, +9.8% growth, ~24% margin) is the growth star. La Roche-Posay, CeraVe, Vichy, SkinCeuticals, and Skinbetter Science have positioned L’Oréal as the science-based skincare leader for dermatologists and health-conscious consumers. This division alone grew faster than the market in 2024 and is expanding into emerging markets—CeraVe’s entry into India and expansion in Sub-Saharan Africa are opening new growth vectors that barely existed a decade ago.

Professional Products

Professional Products (€4.89 billion, +5.0% growth, 22.2% margin) serves hair professionals globally. Kérastase and L’Oréal Professionnel remain dominant, though the salon channel has structural headwinds from at-home coloring and professional fragmentation in digital economies.

The architecture is elegant: Luxe anchors brand prestige and willingness-to-pay; Dermatological drives scientific credibility and premium-mass positioning; Consumer Products distributes volume; and Professional Products maintains salon relationships and trade expertise. Cross-portfolio synergies abound: CeraVe innovations inform Garnier formulations, Lancôme brand prestige elevates Kérastase positioning, and L’Oréal’s centralized R&D feeds all four divisions.

Two acquisitions in 2025 underscore the strategy’s continuation: the €4 billion Kering Beauty transaction (Creed, plus 50-year licenses for Gucci, Bottega Veneta, and Balenciaga fragrances) extends L’Oréal’s foothold in niche perfumery and designer cosmetics, segments where growth and margins are both attractive. The deal also establishes a 50-50 joint venture with Kering to explore longevity and wellness—a category that sits at the intersection of beauty, health, and aging demographics. The Kering deal is emblematic: L’Oréal is no longer just acquiring brands; it is assembling long-term partnerships and option value on emerging wellness categories.

Compared to Safran’s (last’s week article)disciplined exit from low-margin aerospace components, L’Oréal has pursued the inverse strategy: it has entered higher-margin luxury and dermatology, while maintaining market-leading positions in mass beauty. There is no portfolio pruning here, only strategic elevation. The question is not whether L’Oréal can sustain 20% margins—it already does. The question is whether portfolio weight-shifting toward luxury and professional can drive further margin expansion without slowing absolute growth.

Governance: Hieronimus, continuity by stealth, and family alignment

Nicolas Hieronimus has led L’Oréal as CEO since May 2021, arriving with 38 years of tenure in the group—a career arc that mirrors the company’s own: Garnier, International, L’Oréal Paris, and then the selective divisions before the top job. Unlike Patrick Pouyanné at TotalEnergies, Hieronimus speaks softly and leads through execution. His public profile is minimal; his board presence is steady; his capital allocation is methodical. If Safran’s Olivier Andriès embodies “quiet discipline,” Hieronimus embodies “quiet confidence”—the confidence of a man who has seen the company survive Covid, China’s volatility, and the luxury crisis without losing position…

On the family and capital structure front, recent governance shifts signal both continuity and succession planning. In April 2025, Françoise Bettencourt Meyers stepped down from the board after 28 years, passing her seat to her family’s holding company, Téthys, and the vice-presidency to her elder son, Jean-Victor Meyers. The shift is not a retreat; it is a formalization. The Bettencourt family remains the largest shareholder with 34.7% ownership, and their two sons are now embedded in governance. The message is clear: this is a family company, but it is not a family-run company. Professional management—Hieronimus—leads; the family oversees and preserves long-term stewardship. This balance has worked for decades and shows no sign of fracturing.

The board itself reflects institutional maturity: of 15 members, 8 are independent, 2 are Nestlé representatives (reflecting a strategic shareholder relationship from decades past), 3 are from the Bettencourt family, and 2 represent employees. Forty percent are women. The president, Jean-Paul Agon, is a former L’Oréal CEO, lending continuity and strategic perspective.

What distinguishes L’Oréal’s governance from Safran’s is the absence of state involvement. There is no golden share, no French Treasury stake, no defense ministry oversight. Yet this absence has not meant detachment. L’Oréal’s leadership is acutely aware of its role as a French cultural and economic asset; the company has repeatedly affirmed its commitment to French manufacturing, R&D, and employment. The motivation is not state obligation but enlightened self-interest: France’s scientific infrastructure, tax and labor stability, and cultural prestige are competitive advantages L’Oréal guards jealously. Hieronimus’s governance philosophy is thus statecraft without the state—a model of sustainable capitalism where long-term thinking is prized over quarterly optimization.

Financial dynamics: margins, cash generation, and the valuation premium

L’Oréal’s financial profile reads like a textbook in brand-driven profitability. In 2024, the group generated €43.5 billion in revenues, with recurring operating income of €8.7 billion, translating to a 20.0% operating margin—a record. Gross margin stands at 74.2%, up 30 basis points year-over-year, reflecting pricing power, favorable product mix, and operational leverage. For context, Estée Lauder operates at 15% operating margins; Unilever at single digits; Coty and specialty beauty firms cluster around 8-12%. L’Oréal’s 20% is not just premium; it is structural.

Free cash flow reached €6.6 billion in 2024, equivalent to a 15.2% FCF margin—one of the highest in consumer discretionary globally. The company converted 76% of operating income into free cash flow, a signal of capital discipline and minimal working-capital drag. Net cash position strengthened further: L’Oréal now carries more cash than debt, unusual for a company of its size and scope. Balance sheet metrics are fortress-like: net debt to EBITDA is deeply negative (the company has net cash), credit rating is A/A+ stable, and leverage ratios are among the lowest in the sector.

By mid-2025, momentum continued: first-half operating margin expanded to 18.9% on revenues of €23.6 billion, with organic growth of 1.6% and net cash flow of €3.3 billion, signaling resilience even as growth moderates from 2023’s +8% post-Covid surge.

Valuation reflects this premium quality and consistency.

L’Oréal trades at a P/E of ~27.6× (vs. Estée Lauder ~18×), P/S of ~5.0× (vs. sector average ~2-3×), and price-to-book of ~13× (vs. ~8× for peers). These are demanding multiples, yet justified by margins, capital efficiency, and the rarity of such scale with such returns. The market prices L’Oréal as a compounder, and it has behaved like one: revenues have compounded at ~8% CAGR over a decade; operating income at ~12%; and free cash flow at ~10%. For a company of €43.5 billion in revenues, this durability is exceptional.

Shareholder returns reflect this cash generation. Dividend payout in 2024 was €7.00 per share (yield ~1.8-2.0% depending on entry price), up 6.1% year-over-year. L’Oréal has raised dividends for years; the payout ratio remains conservative at ~50% of net income, preserving flexibility for R&D investment, acquisitions (like the Kering deal), and balance-sheet strengthening. The company explicitly signals long-term thinking through its loyalty dividend policy: shareholders holding nominative shares for two or more years receive a 10% boost to their dividend, incentivizing buy-and-hold behavior.

Strategic perspectives: dermatology growth, emerging-market acceleration, and Beauty Tech transformation

L’Oréal’s outlook is constructed around three engines: dermatological skincare growth, emerging-market expansion, and the digitalization of beauty through AI and “Beauty Tech.” Each is backed by quantified momentum.

Dermatological Beauty is the growth flagship. This division grew 9.8% in 2024—double the company average—and is outpacing the overall skincare market, which itself is the largest category in beauty at 39% of the global market. La Roche-Posay is now the third-largest skincare brand globally (all channels), surpassing even heritage leaders. CeraVe has crossed €2 billion in revenues and is expanding internationally at an accelerating pace. Vichy is expanding its haircare line (Dercos) into new geographies. SkinCeuticals and Skinbetter Science grow at double digits year-over-year. Why is this division so dynamic? Several factors: aging demographics drive skin-health spending; dermatological recommendations carry scientific credibility; premium-positioning commands pricing power; and prescription and semi-prescription channels (pharmacies, dermatologist offices) are less price-competitive than mass retail. Emerging markets—India, Brazil, Sub-Saharan Africa—represent vast untapped markets where dermatological skincare is nascent. L’Oréal’s strategy here is offense: CeraVe launches in Mumbai and Delhi are not footnotes; they are beachheads into a market where skin concerns (tropical humidity, pollution) are acute and where dermatological trust is growing.

Emerging markets broadly are re-accelerating. In 2024, emerging markets (Latin America, SAPMENA, Sub-Saharan Africa, and Asean) contributed 16% of group revenues but 36% of growth. By Q1 2025, Latin America was +13.3% and SAPMENA was +12%, far outpacing North America and Europe. China, which contracted in 2024, showed unexpected resilience in Q1 2025 with positive growth again. This geographic rebalancing matters: for a decade, L’Oréal’s growth was yoked to North America and Asie-North (Japan, South Korea); a shift toward India, Brazil, and Africa is not just diversification, but exposure to larger long-term consumption curves. The rising middle class in these regions, urbanization, and social media-driven beauty trends are secular tailwinds. L’Oréal is the best-positioned global player to capitalize on this shift: it has localized R&D (centers in Shanghai, Mumbai, Tokyo), local production, and regional brand architectures (different product lines and positioning for different markets).

Beauty Tech is the strategic pivot. Here is where L’Oréal is spending more heavily than any competitor on transformation. The group invests €1.3+ billion annually in traditional R&D (3% of sales) and an additional €1+ billion in “tech and data” (2% of sales). Translation: L’Oréal is investing 5% of revenues—higher than most of its competitors invest in all operating expenses—on innovation and digitalization.

What does Beauty Tech mean in practice? Three concrete areas:

AI-accelerated research: L’Oréal’s labs use AI to screen molecular compounds, predict efficacy, and simulate formulations. This has compressed research timelines from years to months in some cases. The company announced a strategic partnership with Nvidia in 2025 to deploy generative AI and digital twins for product design, marketing optimization, and virtual testing.

Personalized diagnostics and recommendations: ModiFace (acquired in 2018) enables virtual try-ons; in-store and online kiosks use AI to diagnose skin types and recommend routines. The “Beauty Genius” chatbot on WhatsApp now serves beauty consultations 24/7. This is not gimmickry; it drives conversion and loyalty, and it collects behavioral data that feeds the next iteration of product development.

Sustainable innovation: L’Oréal has deployed BioPod (vertical agriculture) to cultivate rare botanical ingredients with 50% less water; is scaling recyclable packaging (Garnier and DOP ecorecharges); and has achieved Platinum certification by EcoVadis, ranking in the global top 1% for environmental and social performance.

None of this is peripheral. These investments are central to L’Oréal’s thesis for the next decade: as beauty becomes more personalized, data-driven, and conscious, the company that can merge chemistry with code: that can offer AI-powered diagnostics, digital try-ons, and sustainability credentials, will capture premium positioning and pricing.

The forward guidance, while cautious, points to continued outperformance. For 2025, L’Oréal expects market growth of 4-4.5% (vs. +4.5% in 2024), implying deceleration. Yet management has explicitly stated confidence in outperforming: the strategy of emerging-market offense, dermatological growth, and luxury consolidation is designed to deliver 100-200 basis points of market-share gain annually. By 2026-2028, if emerging markets accelerate and luxury stabilizes, L’Oréal could re-accelerate organically to 6-7%, still well above market growth.

France’s stake: L’Oréal as cultural and economic asset

Like Safran, L’Oréal sits at the center of French economic policy, albeit through softer channels. There is no golden share and no Ministry of Beauty. Yet the company is woven into French identity in ways that go beyond shareholder value. L’Oréal is among the largest employers in Île-de-France, operates major R&D facilities in Paris and Chevilly-Larue, and manufactures globally with significant French footprint. When the company announced the Kering Beauty acquisition in October 2025, the French press framed it as a victory for French beauty leadership; when layoffs or site closures are mooted, they trigger swift political response.

The Bettencourt family, stewards of this legacy since Liliane’s inheritance decades ago, have signaled their long-term commitment through Françoise’s own succession planning, the family holding (Téthys), and the sons’ board roles. This is family capitalism at its most sophisticated: a second-generation (Françoise) and third-generation (her sons) transition that preserves identity while enabling professional management. It is a model that works when the alternative, sale to a financial buyer or breakup is politically and emotionally intolerable. The fact that such an arrangement is working smoothly suggests deep alignment between family interest (preserve the L’Oréal brand and its French heritage) and shareholder interest (maximize returns).

When family and capital interests diverge, chaos usually follows; here, they appear synchronized.

Investment thesis

L’Oréal is a structural play on global consumer wealth, emerging-market expansion, and the digitalization of beauty through AI and personalization. With 20% operating margins, €6.6 billion in free cash flow, and 42% global market share, it has built a durable competitive moat rooted in brand portfolio breadth, scientific credibility (R&D spending), and operational excellence. The company is outperforming its market by 100-200 basis points annually, a cadence likely to continue as dermatological beauty (9.8% growth in 2024) and emerging markets (36% of growth contribution) accelerate. Valuation is demanding (P/E ~27×, P/S ~5.0×), but justified by consistency, growth-for-dollar, and the rarity of such a combination in a category (consumer discretionary) where competition is intense. For investors seeking exposure to luxury, innovation, and emerging consumer spending growth, with a large, profitable, and sustainably advantaged franchise, L’Oréal is a long-duration compounder priced as a champion and delivering like one.

Disclaimer: This publication is provided for informational and educational purposes only and does not constitute investment advice, a recommendation, or a solicitation to buy or sell any financial instruments. The analysis and opinions expressed are those of the author at the time of writing and are subject to change without notice. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions. The author assumes no responsibility for any losses that may result from reliance on this information.